BEL’s record ₹26,750 crore turnover for FY26 is probably the best news this stock will see for the next eighteen months — and the market is celebrating it like it’s the beginning of something rather than the end.

That’s the read worth sitting with before the 6% pop off the announcement fades into the background noise of a broader market that has been correcting since January. The NIFTY 50 fell from 26,146 in January 2026 to 22,760 by April 1, per Yahoo Finance. BEL at ₹422.7 remains 11% below its 52-week high of ₹473.5, also per Yahoo Finance. Those two numbers together don’t tell a story of a stock finding its floor. They tell a story of a stock that hasn’t convinced the market the rally deserves to continue.

The obituary right now is almost entirely constructive. Record turnover. Defense sector momentum. PSU rotation as risk appetite dries up elsewhere. Garden Reach Shipbuilders rallying. HAL with similar numbers. The story writes itself — India’s defense modernization is a decade-long structural theme, BEL is a core beneficiary, and the record top line confirms everything the bulls said it would.

The problem with a narrative that writes itself is that everyone has already written it.

The Silent Cost Nobody Is Discounting

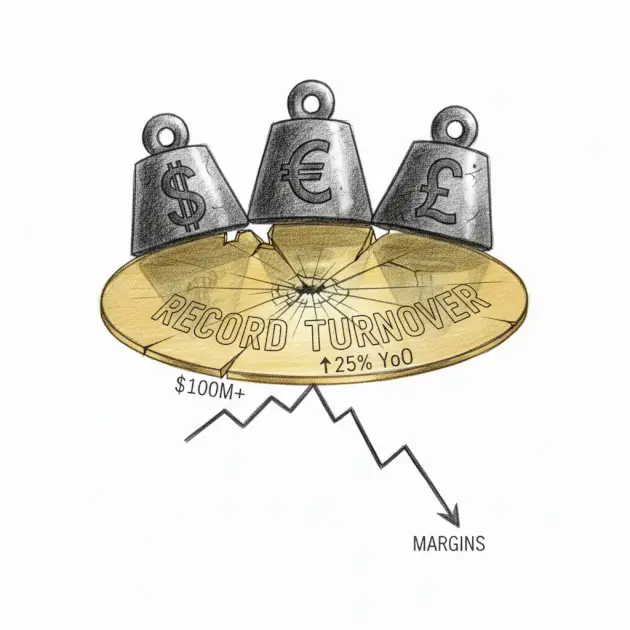

Per ExchangeRate-API data as of April 1, 2026, the Indian rupee is trading at approximately ₹93.8 against the US dollar. For a defense electronics firm whose imported sub-assemblies — semiconductors, specialized sensors, high-precision components — typically account for 25 to 35% of total project costs, that exchange rate isn’t a footnote. It’s a margin event in slow motion.

The mechanism is straightforward. Defense contracts in India are largely fixed-price agreements, often negotiated years before delivery. When BEL signs a contract with the Ministry of Defence at a certain project cost, the rupee-dollar assumption baked into that pricing may have been substantially different from where the currency sits today. There is no clean pass-through mechanism. The rupee depreciates, the import bill rises in rupee terms, and BEL absorbs the difference. Record turnover at the top line can coexist with quietly deteriorating margins at the bottom — and the FY26 announcement, as reported, is a turnover figure. Margin data is where the real answer lives, and that story hasn’t been fully told yet.

The weakest assumption in this entire argument is the import-cost ratio itself — BEL has been actively indigenizing its supply chain, and the actual share of dollar-denominated inputs could be lower than the 25-to-35% range commonly cited for defense electronics. But even at the lower bound, a currency move of this magnitude on fixed-price contracts leaves a mark.

What a High Base Actually Means

There’s a particular kind of market euphoria that arrives when a company crosses a round-number milestone. ₹26,750 crore sounds like acceleration. Functionally, it is a new denominator against which every future quarter gets measured. The company now has to grow from here — and “from here” is a record high set in a fiscal year that benefited from a concentrated burst of order execution, broad defense sector tailwinds, and a government spending cycle that may not replicate at the same intensity.

When every major participant in a sector reports record figures in the same reporting window — BEL on turnover, HAL on earnings, Garden Reach on order intake — the instinct is to read it as confirmation of a structural theme. The alternative reading is that you’re watching the simultaneous peak of an execution cycle, not the start of a new one. Order books get executed. Pipelines need refilling. And the next generation of defense tenders, increasingly structured under multi-vendor procurement frameworks designed to introduce competitive pricing, represents a different competitive environment than the one that produced these numbers.

BEL’s historical advantage rested substantially on its status as a preferred production partner — embedded relationships, established manufacturing infrastructure, institutional familiarity with MoD procurement timelines. That advantage is real and durable in the near term. But as private-sector defense entrants mature their production capabilities and the government leans harder into competitive bidding to control costs, the pricing power that has supported BEL’s margin profile faces a structural test that doesn’t show up in a single FY turnover headline.

The 11% gap between BEL’s current price and its 52-week high is being framed by most analysts as a discount. The contrarian position is that it’s the market quietly doing the math on what comes after a record year and not fully liking the answer.

The rotation into PSUs during the broader NIFTY correction adds complexity. Defensive flows into stable government-linked entities are a real phenomenon in risk-off environments, but they’re not the same as fundamental revaluation. When risk appetite returns, those flows reverse. BEL catching a bid because it looks stable relative to small-cap carnage is a different proposition than BEL catching a bid because investors see a clear path to margin expansion from this level.

Here is the ugly truth. None of this makes BEL a broken company. The order book remains substantial. The defense modernization theme is not imaginary. The government’s commitment to indigenous defense production creates a durable demand floor that many sectors would envy. The question isn’t whether BEL is a good company. The question is whether ₹422.7 — or any price near the 52-week high — correctly prices what the next eighteen months actually look like: a high base, a weakening rupee quietly compressing margins on fixed-price legacy contracts, and a competitive landscape that is incrementally less favorable than the one that produced today’s record.

A record turnover is a fine thing to report. It’s also, historically, the single most reliable moment to start asking what the company does for an encore — because the market, for a brief window, has stopped asking that question entirely.

Congratulations on hitting a record. Now explain how you top it while the rupee sits at 93.8 and the next round of tenders goes to the lowest bidder.